Consumer travel spending sentiments are turning cold. As Japan travel plunged under the influence of `No Japan,` not only Japan but also overall overseas travel spending is shrinking. Domestic travel has also declined without reflecting benefits, bringing a cool wind throughout the tourism industry.

`Weekly travel behavior and planning study` (the sample size of 300 a week or 14400 a year in 2016, and 500 a week or 26000 a year since 2017), conducted by travel specialized research firm, ConsumerInsight, asked consumers about any likely changes in both domestic and overseas travel spend in the next year and analyzed its results. "Travel spending intention" is a response rate for `will increase (very much or slightly)` in their next year travel spend when asked.

■ Travel spend intention continues to fall

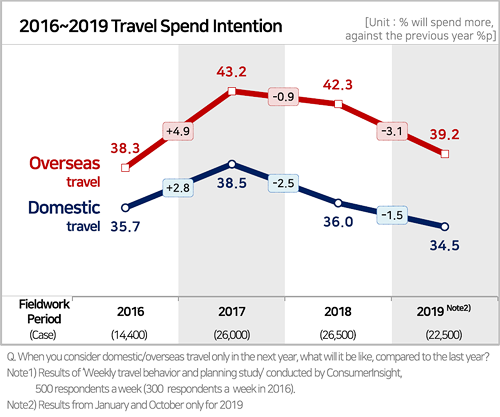

The intention to spend travel expenses soared in 2017, when there were two long holidays (alternating holidays in May and Chuseok holidays in October). The figure rose by 4.9 percentage points(%p) and 2.8%p, respectively, to the record high of 43.2% for overseas and 38.5% for domestic travel [Figure 1]. In the next year, 2018, the overseas travel remained flat at 42.3% (-0.9%p), while the domestic travel dropped to 36.0% (-2.5%p), returning to its 2016 level on travel spend. Although 2019 is not yet finalized, the survey results from January to October showed that the intention to spend overseas travel this year was 39.2%, down 3.1%p year-on-year. The rate of decline is almost four times that of last year (0.9%p). Meanwhile, domestic travel spending intentions fell by 1.5%p to 34.5%, falling for the second consecutive year following 2.5%p last year.

[Figure1] Domestic and Overseas Travel Expenditure Intention

■ Overseas travel sentiments failing to recover from the chill of `No Japan`

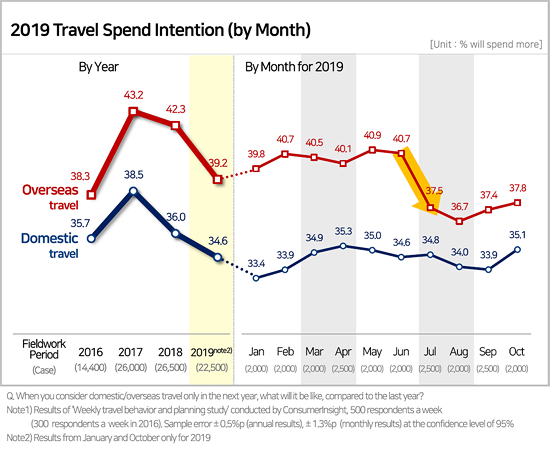

2019 monthly results clearly show changes in consumers` travel sentiments in the wake of `No Japan` [Appendix]. The intention to spend on overseas travel from January to June was unchanged at around 40% (39.8 ~ 40.9%). However, in July, travel sentiments towards Japan, a popular overseas travel destination, cooled rapidly, and the intention to spend on overseas travel fell by 3.2%p to 37.5%. This is the lowest in 37 months since May 2016 (33.3%), and there is no sign of a reversal until October, three months later since then. On the other hand, domestic travel spending intentions remained flat over the last 10 months in 2019.

The impact of the No Japan movement on the overall travel market was greater than expected. Although travel demand has been largely replaced by regions outside Japan, such as Southeast Asia, it has continued to fall by more than 3%p.

The intention to increase spending more overseas than in domestic increased from 4.7%p in 2017, to 6.2%p in 2018. In addition to long-term holiday seasons, the burden of airfare has diminished due to the expansion of low-cost carriers(LCC), and the popularity of short-distance trips, including Japan, Taiwan, and Vietnam, has increased short-term travel, turning consumers towards overseas travel rather than domestic travel.

The ever increasing gap in consumers’ intention to spend abroad against domestically has narrowed and returned to the 2017 level difference (4%p), but it is rather unfortunate that domestic travel failed to enjoy any reflecting benefits from the shrink of overseas travels. The main reason for this is the shrinking consumer sentiments due to the economic recessions, and consumers’ evaluation of overseas travel as `more value for money` also has a great influence on the current situations. It is not easy to turn consumers’ back once they turned away. Only when the competitiveness of domestic travel gets improved, only then we can catch back the rabbits that have left their home.

[Appendix] 2019 Travel spend intention (by month)

|